Nissan Leaf Insurance Rates

Enter your zip code below to view companies that have cheap auto insurance rates.

UPDATED: May 14, 2024

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident car insurance decisions. Comparison shopping should be easy. We are not affiliated with any one car insurance provider and cannot guarantee quotes from any single provider.

Our insurance industry partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

Editorial Guidelines: We are a free online resource for anyone interested in learning more about auto insurance. Our goal is to be an objective, third-party resource for everything auto insurance related. We update our site regularly, and all content is reviewed by auto insurance experts.

U.S. average insurance rates for a Nissan Leaf are $1,256 a year with full coverage. Comprehensive costs approximately $234 a year, collision insurance costs $400, and liability coverage costs $464. Liability-only insurance costs as little as $514 a year, and high-risk driver insurance costs around $2,722. Teen drivers pay the highest rates at up to $4,858 a year.

Average premium for full coverage: $1,256

Price estimates by individual coverage:

Rate estimates include $500 physical damage deductibles, 30/60 split liability limits, and includes medical/PIP and uninsured motorist coverage. Estimates are averaged for all U.S. states and Leaf trim levels.

Price Range from Low to High

For a driver in their 40's, Nissan Leaf insurance prices range from as low as $514 for liability-only coverage to a high of $2,722 for a high-risk insurance policy.

Geographic Price Range

Your location has a large influence on the price of insurance. Rural locations have a lower frequency of collision claims than larger metro areas. The diagram below illustrates how location helps determine auto insurance prices.

The ranges above demonstrate why it is important to compare rates using their specific location and risk profile, rather than using price averages.

Use the form below to get customized rates for your location.

Enter your zip code below to view companies based on your location that have cheap auto insurance rates.

Additional Charts and Tables

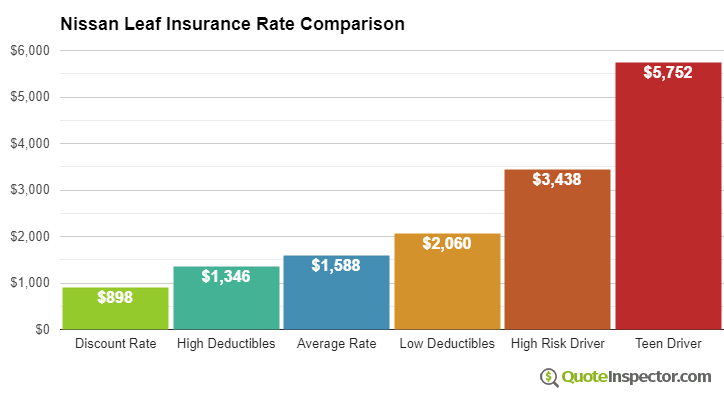

The chart below details average Nissan Leaf insurance rates for additional coverage and risk scenarios.

- The lowest rate with discounts is $734

- Drivers who choose higher $1,000 deductibles will pay $1,112 annually

- The average rate for the average middle-age driver who chooses $500 deductibles is $1,256

- Choosing low $100 deductibles for comprehensive and collision insurance will increase the cost to $1,534

- High-risk insureds with multiple violations and an at-fault accident could pay around $2,722

- The price for full coverage for a teenage driver can cost $4,858 a year

Car insurance prices for a Nissan Leaf are also quite variable based on your driving record, the trim level and model year, and physical damage deductibles and liability limits.

Older drivers with no driving violations and high deductibles may only pay around $1,200 per year on average for full coverage. Prices are highest for teenage drivers, where even good drivers will be charged in the ballpark of $4,800 a year. View Rates by Age

The state you live in makes a big difference in Nissan Leaf insurance rates. A 40-year-old driver could pay as low as $910 a year in states like Utah, Ohio, and New Hampshire, or as much as $1,700 on average in New York, Michigan, and Florida.

| State | Premium | Compared to U.S. Avg | Percent Difference |

|---|---|---|---|

| Alabama | $1,136 | -$120 | -9.6% |

| Alaska | $962 | -$294 | -23.4% |

| Arizona | $1,044 | -$212 | -16.9% |

| Arkansas | $1,256 | -$0 | 0.0% |

| California | $1,432 | $176 | 14.0% |

| Colorado | $1,200 | -$56 | -4.5% |

| Connecticut | $1,292 | $36 | 2.9% |

| Delaware | $1,422 | $166 | 13.2% |

| Florida | $1,572 | $316 | 25.2% |

| Georgia | $1,160 | -$96 | -7.6% |

| Hawaii | $902 | -$354 | -28.2% |

| Idaho | $848 | -$408 | -32.5% |

| Illinois | $936 | -$320 | -25.5% |

| Indiana | $946 | -$310 | -24.7% |

| Iowa | $848 | -$408 | -32.5% |

| Kansas | $1,194 | -$62 | -4.9% |

| Kentucky | $1,714 | $458 | 36.5% |

| Louisiana | $1,860 | $604 | 48.1% |

| Maine | $774 | -$482 | -38.4% |

| Maryland | $1,036 | -$220 | -17.5% |

| Massachusetts | $1,006 | -$250 | -19.9% |

| Michigan | $2,182 | $926 | 73.7% |

| Minnesota | $1,050 | -$206 | -16.4% |

| Mississippi | $1,504 | $248 | 19.7% |

| Missouri | $1,114 | -$142 | -11.3% |

| Montana | $1,348 | $92 | 7.3% |

| Nebraska | $990 | -$266 | -21.2% |

| Nevada | $1,506 | $250 | 19.9% |

| New Hampshire | $904 | -$352 | -28.0% |

| New Jersey | $1,402 | $146 | 11.6% |

| New Mexico | $1,112 | -$144 | -11.5% |

| New York | $1,322 | $66 | 5.3% |

| North Carolina | $724 | -$532 | -42.4% |

| North Dakota | $1,028 | -$228 | -18.2% |

| Ohio | $868 | -$388 | -30.9% |

| Oklahoma | $1,290 | $34 | 2.7% |

| Oregon | $1,150 | -$106 | -8.4% |

| Pennsylvania | $1,198 | -$58 | -4.6% |

| Rhode Island | $1,678 | $422 | 33.6% |

| South Carolina | $1,138 | -$118 | -9.4% |

| South Dakota | $1,060 | -$196 | -15.6% |

| Tennessee | $1,100 | -$156 | -12.4% |

| Texas | $1,516 | $260 | 20.7% |

| Utah | $930 | -$326 | -26.0% |

| Vermont | $862 | -$394 | -31.4% |

| Virginia | $752 | -$504 | -40.1% |

| Washington | $970 | -$286 | -22.8% |

| West Virginia | $1,150 | -$106 | -8.4% |

| Wisconsin | $870 | -$386 | -30.7% |

| Wyoming | $1,120 | -$136 | -10.8% |

Choosing high deductibles could save up to $430 a year, while buying higher liability limits will push prices upward. Moving from a 50/100 limit to a 250/500 limit will increase prices by as much as $417 extra every 12 months. View Rates by Deductible or Liability Limit

If you have some driving violations or tend to cause accidents, you may be forking out anywhere from $1,500 to $2,100 extra each year, depending on your age. A high-risk auto insurance policy can cost around 43% to 133% more than average. View High Risk Driver Rates

| Model Year | Comprehensive | Collision | Liability | Total Premium |

|---|---|---|---|---|

| 2024 Nissan Leaf | $346 | $660 | $390 | $1,554 |

| 2023 Nissan Leaf | $332 | $656 | $398 | $1,544 |

| 2022 Nissan Leaf | $320 | $640 | $416 | $1,534 |

| 2021 Nissan Leaf | $310 | $612 | $430 | $1,510 |

| 2020 Nissan Leaf | $292 | $592 | $442 | $1,484 |

| 2019 Nissan Leaf | $282 | $548 | $452 | $1,440 |

| 2018 Nissan Leaf | $270 | $516 | $456 | $1,400 |

| 2017 Nissan Leaf | $258 | $464 | $460 | $1,340 |

| 2015 Nissan Leaf | $234 | $400 | $464 | $1,256 |

| 2014 Nissan Leaf | $228 | $374 | $474 | $1,234 |

| 2013 Nissan Leaf | $210 | $346 | $474 | $1,188 |

| 2012 Nissan Leaf | $206 | $314 | $478 | $1,156 |

| 2011 Nissan Leaf | $192 | $288 | $474 | $1,112 |

Rates are averaged for all Nissan Leaf models and trim levels. Rates assume a 40-year-old male driver, full coverage with $500 deductibles, and a clean driving record.

How to Find the Best Nissan Leaf Insurance

Getting lower rates on auto insurance not only requires being a safe and courteous driver, but also having above-average credit, avoid buying unnecessary coverage, and attention to physical damage deductibles. Invest time comparing rates at least every other year by requesting quotes from direct companies like Progressive and GEICO, and also from several local insurance agents.

Below is a brief recap of the car insurance concepts covered in the charts and tables above.

- Drivers who tend to receive serious violations pay on average $1,470 more per year for auto insurance

- You may be able to save around $150 per year just by quoting early and online

- Increasing physical damage deductibles can save around $425 each year

- Consumers who purchase higher levels of liability will pay about $510 every year to go from a low limit to 250/500 limits

Rate Tables and Charts

Rates by Driver Age

| Driver Age | Premium |

|---|---|

| 16 | $4,858 |

| 20 | $2,896 |

| 30 | $1,294 |

| 40 | $1,256 |

| 50 | $1,150 |

| 60 | $1,128 |

Full coverage, $500 deductibles

Rates by Deductible

| Deductible | Premium |

|---|---|

| $100 | $1,534 |

| $250 | $1,406 |

| $500 | $1,256 |

| $1,000 | $1,112 |

Full coverage, driver age 40

Rates by Liability Limit

| Liability Limit | Premium |

|---|---|

| 30/60 | $1,256 |

| 50/100 | $1,349 |

| 100/300 | $1,465 |

| 250/500 | $1,766 |

| 100 CSL | $1,395 |

| 300 CSL | $1,650 |

| 500 CSL | $1,836 |

Full coverage, driver age 40

Rates for High Risk Drivers

| Age | Premium |

|---|---|

| 16 | $6,900 |

| 20 | $4,620 |

| 30 | $2,764 |

| 40 | $2,722 |

| 50 | $2,600 |

| 60 | $2,578 |

Full coverage, $500 deductibles, two speeding tickets, and one at-fault accident

If a financial responsibility filing is required, the additional charge below may also apply.

Potential Rate Discounts

If you qualify for discounts, you may save the amounts shown below.

| Discount | Savings |

|---|---|

| Multi-policy | $66 |

| Multi-vehicle | $67 |

| Homeowner | $20 |

| 5-yr Accident Free | $87 |

| 5-yr Claim Free | $81 |

| Paid in Full/EFT | $53 |

| Advance Quote | $60 |

| Online Quote | $88 |

| Total Discounts | $522 |

Discounts are estimated and may not be available from every company or in every state.

Compare Rates and Save

Find companies with the cheapest rates in your area